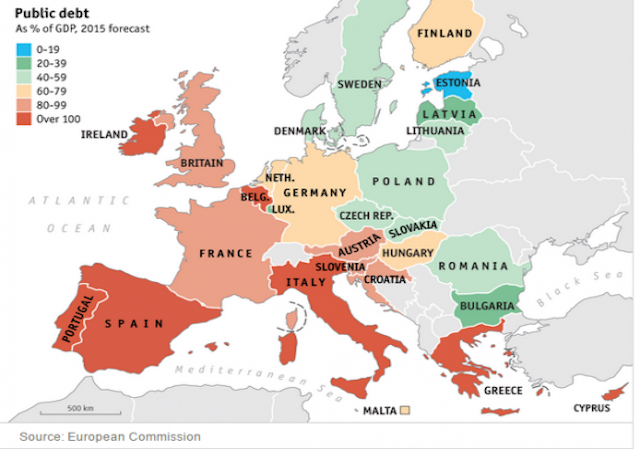

Greece and Eurozone Talks Stall as Deadline Looms

on June 27, 2015

10 Comments

Greece and the Eurozone have been unable to reach an agreement ahead of a bailout deadline which quickly approaches on June 30th. If negotiations fail, Greece could leave the European Union and ultimately face economic collapse.

The situation is already causing a dash for cash in the debt strapped country.

Bloomberg reports:

Greeks Line Up at Banks and Drain ATMs as Tsipras Calls Vote Some Greek banks were beginning to limit cash transactions as hundreds of people lined up outside branches and drained cash machines after Prime Minister Alexis Tsipras called a referendum that could decide his country’s fate in the euro. Two senior Greek retail bank executives said as many as 500 of the country’s more than 7,000 ATMs had run out of cash as of Saturday morning, and that some lenders may not be able to open on Monday unless there was an emergency liquidity injection from the Bank of Greece. A central bank spokesman said it was making efforts to supply money to the system.