3 Ways Chuck Schumer’s Airfare Probe Ignores Economic Realities

Economic populism relies on disregarding reality

Last week, Senator Chuck Schumer (D-NY) said he wants the Department of Justice and the Department of Transportation to investigate why airfares are not decreasing along with falling oil prices.

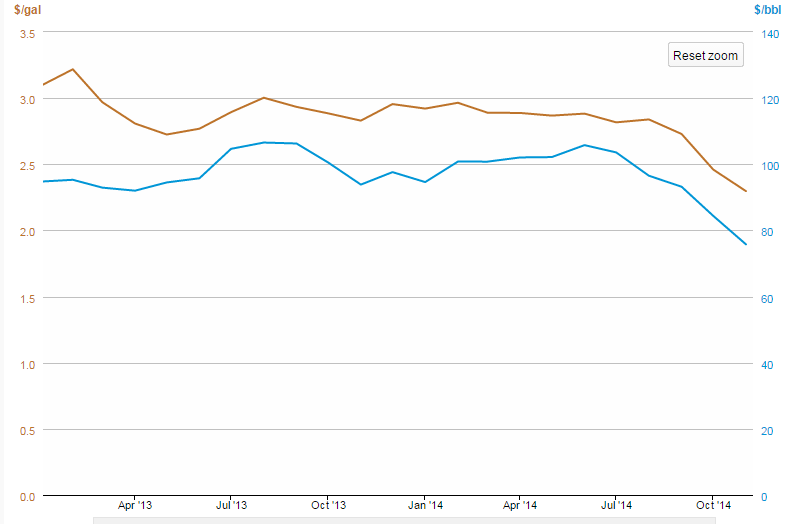

On the surface, Schumer’s observation makes sense. Crude oil and jet fuel prices are strongly correlated, and on average jet fuel comprises a third of airlines’ operating expenses. As such, the declining cost of oil, and therefore jet fuel, should reduce airlines’ expenses, thereby giving them the opportunity to charge lower airfares to consumers.

Chart from U.S. Energy Information Administration. Blue is WTI crude oil, orange is jet fuel.

The key word here is “opportunity.” Even though Schumer says “it’s safe to say that the airlines can afford to pass at least some of these savings onto the consumer,” reality is far from this populist idealism.

The airlines’ first obligation is to their shareholders and employees, who have legitimate claims to these savings in the forms of higher dividends and wages. Then there is the issue of the government telling private businesses how they should set their prices—as if Washington bureaucrats know the first thing about airline pricing strategy, arguably the most complex in existence.

Economic philosophy aside, there are serious flaws with the rationale underlying Schumer’s desired investigation. These flaws are the result of an utter disregard—whether by design or by way of tremendous ignorance—of the financial and economic realities of the airline industry of present, past, and near-term future.

1. Airline Fuel Hedging

With oil prices trending toward a 50% decline this year, one would expect to hear the airlines breathe a collective sigh of relief as the pressure on their bottom lines eased. After all, airlines operate on razor-thin profit margins of 2.4%, or about $5.42 per passenger, according to Tony Tyler, CEO of International Air Transport Association (IATA). Compare that to the S&P 500’s average profit margin of 9.5%.

However, because they engage in fuel hedging, most airlines have not experienced any savings this year and, most likely, will not in the short-term. Fuel hedging refers to the variety of investment strategies an investor, speculator, or company can use to lock-in a predetermined price for a future purchase of fuel or use to obtain the option to do so. These various hedges basically act like insurance policies that pay out if fuel prices rise above a certain level.

All major domestic airlines, except American Airlines and Allegiant Travel, use fuel hedging, and thus entered this bear market for oil with a lot of money tied up in the expectation that oil prices would instead be rising (or remain at current high levels).

So, some airlines are even losing money right now. Depending on the type of fuel hedging strategy, the airlines have to either write down the defunct hedges as losses or exercise them and purchase fuel at above-market prices. For example, Delta announced that despite estimated cost savings of $1.7 billion for 2015, it would have to write-down a $1.2 billion loss for its useless fuel hedges.

2. Rising Demand for Air Travel

Airlines are spending major amounts this year and next to upgrade their fleets and terminals and buy new planes. Why? Demand for air travel is growing and is slated to increase further. The growing demand also helps to explain high ticket prices.

IATA estimates that the airline industry’s 2015 profit will be $25 billion, up from $19 billion this year (up from the $18 billion estimated before the precipitous fall in oil prices). Falling fuel prices not only buttress airlines’ bottom lines, they induce increased consumer spending, which inevitably will include more air travel. Most of this buoy in demand will come from North America.

3. Incentives (Or Lack Thereof)

Economics is all about incentives. What incentives do the airlines have to reduce ticket prices? None. Why should companies with sky-high debt and a history of bankruptcies and bailouts not want to expand their profit margins whenever possible, and when, as demonstrated in the previous point, it is economically viable to do so?

In fact, no company or industry acts against their profit-maximizing motives. Airlines for America, an industry trade group, released a statement challenging Schumer. In it they write, “Airlines should be treated like every other business. When the price of coffee beans falls, no one asks Starbucks why his or her latte does not cost less. You want Starbucks to expand its stores and products, give back to its baristas, and reward investors. Airlines are no different.”

Furthermore, airline executives know the glut in oil prices isn’t guaranteed in the long-term, and not necessarily even in the short-term. Changes in national economic policy, politics, war/terrorism, and weather all play roles in determining oil prices, and airlines would rather improve their cash stockpiles now than find themselves in a serious bind later.

In his zeal to expand the role of government in private commerce, Schumer has selected easy prey. For mostly legitimate reasons, airlines get a pretty universal bad rap; it is unsurprising many are not rushing to their defense.

But just because we’ve all had more than one or two bad experiences with airlines, don’t jump on Schumer’s populist bandwagon without looking at the economic facts. Despite his dual degrees from Harvard, Schumer has not spent one minute of his professional life working in the private sector, let alone the airline industry.

It seems the old quip that goes “those who can, do; those who can’t, teach” should be changed to “those who can, do; those who can’t, legislate.”

Donations tax deductible

to the full extent allowed by law.

Comments

Oh joy, more lectures from our lessers who have never ran a business (and…No Dumba$$, ‘running’ a campaign is not ‘running a business’).

Why not investigate oil companies when gas historically goes up in summer and down in winter, regardless of crude prices?

I’d be a lot happier if chuckie would investigate the TSA and leave private business alone.

that 5$ /pass is actually a pretty high end number too, amr eagle was pennies to 70 cents per passenger and we had 180 or so aircraft.

besides, why SHOULD they lower the price? every time they turn around they have to deal with union demands and need to maintain a buffer for that.

I ever tell you about the time we caught an a/c inspector paperwhipping the metal inspections on airframes and when we tried to fire him we got blamed for racism? and the union won the fight as the court date was set on a date a prime witness was having cancer surgery. judge very pro-union and refused to accommodate.

yeah I don’t fly anymore for a reason.

First things first. Chucky should be looking for ways to reduce the cost of goverment e.g., delete at least one government agency a year. Recall a de Blasio per year, too.

Chucky should stop messing with the marketplace. Nothing happens in isolation. Nothing. The ‘little man’ that he pretends to be looking out for may have airline company equities within his retirement fund. The world doesn’t rotate around Chucky.

I thought I heard once that airlines buy their fuel a few months ahead of time so they won’t run out. So, the jet-A they’re burning now was purchased at the price of three months ago. That means their cost won’t go down until they’re burning the fuel they buy today.

Is this true? Or am I remembering incorrectly?

JohnC, you are correct.

There are numerous ways to fuel hedge, but you can divide most (read: not all, but most) strategies into two categories: futures contracts and options contracts. The essential difference is that a futures contract must be executed, whereas an options contract merely gives the buyer an option to exercise.

Let’s say today the gas price is $1.00, and you expect it to rise six months later to $1.50.

Scenario 1–Futures Contract:

Airline A purchases a futures contract that allows it to purchase fuel at a pre-determined price of $1.25 in six months. If the price rises above $1.25 + price of contract, Airline A benefits. If the price remains below $1.25 + price of contract, Airline A loses. Since this is a futures contract, it must be executed; therefore, at that six month, Airline A is using fuel that costs more than the market price.

Scenario 2–Options Contract:

Pretty much everything remains the same, except at that six month, Airline A has merely the option to purchase the fuel at $1.25. If the market price is below that, Airline A would rather not exercise the option and just write-down he loss, as Delta did.

I’m going to say you’re wrong, Casey.

A lot of people…A LOT…who trade in futures contracts are NEVER, EVER going to take or give delivery of a commodity.

A LOT of people who deal in pork bellies futures are Jews. So…REALLY…!?!?!

The futures market is entirely a market based on a fiction, but it is one that serves a TREMENDOUSLY important function. It allows both producers and consumers (that is those who will use a product as an important factor of THEIR production) to avoid the full brunt of the CASH market price fluctuations for a given commodity.

NOBODY who deals in pork belly futures EXPECTS or even WANTS their futures contract to be realized with actual delivery.

As an example, if I run a feed-lot (which is most often a Ph.D.-level guy with VERY sophisticated information) I will buy or sell futures for sorghum, corn, and molasses. I will buy or sell futures for feeder cattle (one of my in-puts) and for fed cattle (my out-put). Whether I buy or sell DEPENDS on whether I think the cash market will rise or fall for the particular commodity relative to my position. I will NEVER deliver sorghum, corn or molasses. I will simply sell those futures at the market rate (which will pretty much be the cash rate) at some point before they come due, or even when they come due.

The gist of this whole system is that it allows producers or consumers to shave off the HUGE deltas in the cash markets. This is IMMENSELY important and utilitarian.

I am surprised to see the example of Delta, given that they own their own oil refinery.

Even if one owns a refinery it’s still necessary to buy the crude and pay all of the costs associated with refining and delivering the finished product

Their refinery capacity isn’t close to what they need to supply all their needs. It is there to soften the effect of the “crack spread” during the autumn and spring.

Since airlines are semi-public, inasmuch as they need government license to operate We-the-People’s airspace, some government investigation seems legitimate. Whether it’s worthwhile is an entirely different question, but I’ll give the benefit of the doubt to my betters and elders.

“but I’ll give the benefit of the doubt to my betters and elders.”

Bend over.

You’re overpaid says this elder.

Being older doesn’t make one an “elder”, and being elected doesn’t make one “better”.

Use your own brain. Does Schumer’s statement still make sense, after you factor in all the information posted here?

While the government should not be in the business of fixing prices for any private corporation, the government should be in the business of preventing monopolistic practices and encouraging competition. Airlines are merging into megacarriers with less and less competition. When was the last time a new airline was started and undercut the prices at the majors? How long ago was People Express? The airlines have done everything possible to torture their customers and will continue to do so as long as the government says “United and Continental merge…sure”.

Chuckie Schumer is a typical fake populist Democrat. He takes money, a lot of money, wherever he can get it, and then rails, like this about some industry or another gouging consumers.

Hey Chuck, get rid of some of the barriers to entry and maybe there would be some competition. We do have an oligopoly at this point and that’s not healthy.

Remember, Schumer pulled this same stunt in 1995 about breakfast cereal prices, of all things. He wanted a Justice Department investigation into the prices of Raisin Bran and Cap’n Crunch, among others.

I am not making this up. Google: Schumer cereal prices

“Economic populism relies on disregarding reality”

Wrong. 1%er exploitation relies on disregarding the reality that 1%ers do nothing, create nothing, make nothing, and are useless parasites on the economic activity of the middle and lower classes. They, the 1%ers, most certainly didn’t build it; we did.

Tell that to Steve Jobs.

You just NEVER get tired of showing that stupid ass, do ya?

The federal government is a major consumer of oil based products.

Will Senator Schumer propose an adjustment of the recently passed federal spending bill to adjust the estimated federal expenditures downward by the estimated savings from the oil price drop? Will he propose a tax credit to taxpayers in the amount of the estimated oil price savings? Will he propose a credit earmarked for deficit reduction for the amount of the estimated federal fuel cost savings?

Senator Schumer has had-it-out for the airlines ever since a flight attendant told him he had to turn off his cell phone. [Key words search for: Schumer apologizes to flight attendant].

bGeorge, I was wondering why Schumer decided to pick on the airlines. Thanks for Google search suggestion.

Matthew 7:5 – “You hypocrite, first take the log out of your own eye, and then you will see clearly to take the speck out of your brother’s eye”.

Chuckie Schmooah is the Poster Boy for Repealing the 17th Amendment.

The dumb SOB watched over-capacity airlines eviscerate one another through post-deregulation with fare wars which, while good for consumers, was bad for airlines. All the while, more and more new regulations, the need to upgrade aging fleets and rising fuel prices threatened to sink the airlines forever in a sea of red ink.

When the industry finally sorts itself out and starts making money for the first time since deregulation, Chuckie wants to de-facto, re-regulate it.

When people stop flying, fares will come down. When people stop buying 300-dollar Air Jordans, the price will come down. When people stop buying i-phones and the required new-charger-of-the-year, prices will come down. When people stop buy 50-million dollar Manhattan (not Kansas) apartments, prices will come down.

Instead of Karl Marx, Progressocrats need to read Adam Smith.

See, this is how progressives twist the knife of their own past failures into something that sounds popular and just to the low info voter. It is very similar to the living wage campaigns but on the other side of the government interference plague.

The unions have nearly killed the airline industry. They were operating on razor thin profit margins because of ridiculous bloat and federal overreach.

Schumer is ABSOLUTELY RIGHT that airlines SHOULD be able to pass on fuel cost savings to their consumers and thereby raise profits through volume. What he fails to see is that progressive politics and federal oversight have pushed that market into its current sorry state…same as the USPS (which also hasn’t seemed to pass on its recent savings to consumers).

Airline travel is still optional for a large portion of this country. Therefore, volume is key to raising overall profit margins. If airlines COULD, they WOULD. It’s really that simple.

Excellent point about volume driving profits.

I was originally going to have this paragraph in my piece, but I took it out because I was unsure of its validity:

“Some might wonder why American and Allegiant just don’t go ahead and decrease their airfares slightly, since they can afford to do so, in order to steal market share from the other airlines. Theoretically, they could. But even if they were to achieve 100% capacitance on every flight, there are more flyers than these two airlines can seat; these flyers would resort to the other airlines, who, because American and Allegiant are already at 100% capacity, would have no incentive to reduce their airfares. So while fascinating, this is mostly a mute point.”

I’m wondering what your thoughts on this rudimentary game-theoretic analysis are?

… Despite his dual degrees from Harvard, Schumer has not spent one minute of his professional life working in the private sector, let alone the airline industry.

It seems the old quip that goes “those who can, do; those who can’t, teach” should be changed to “those who can, do; those who can’t, legislate.”

More an example of a point I like to make with intellectuals often. A degree means you are educated, it doesn’t necessarily mean you are intelligent. Some of the smartest and most well-read people I know have only a high school diploma. And many a moron I know has the term doctorate behind their name.