Will the Fed Raise Rates in 2015?

Count on it happening later rather than sooner—if at all

Entering 2015, most economists expected that the Federal Reserve would finally begin raising short-term interest rates. Fewer than two weeks in to the year and that thesis is already beginning to crumble.

For seven years, the Fed kept interest rates at rock-bottom levels and employed a massive money-printing program called Quantitative Easing in the hopes of boosting the money supply, expanding credit, and causing inflation to jump-start the economy (so the theory goes). Many experts have long waited for the Fed to “normalize” policy and raise rates, for reasons that include a desire to stop expanding the money supply, and wanting the Fed to have a cushion to lower them once again when another crisis occurs.

While credit finally appears to be coming more available, neither the mild-mannered inflation the Fed wanted nor the rampant hyperinflation Fed detractors prophesied has materialized.

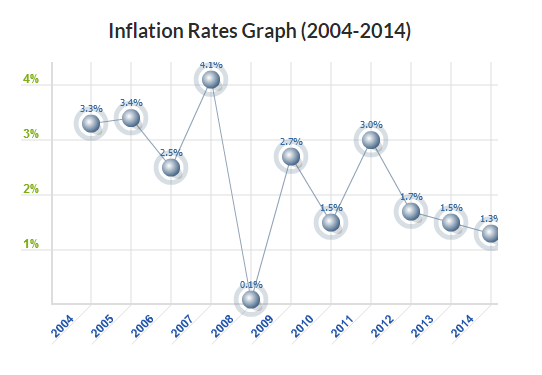

In 2014 the CPI inflation rate was 1.3%, the lowest since 2008. However, most economists, including those at the Fed, like to see 2% inflation.

Graph from www.usinflationcalculator.com.

Inflation has decreased every year since 2011, when it registered at 3%, and hasn’t been at or above the 2% target since then. This trend does not inspire confidence in Fed policy makers to increase rates right now.

Still, the minutes released by the Fed on Jan. 7 indicate the Fed does not need to see 2% inflation to begin raising rates. What they do indicate is that the Fed will not raise rates until it becomes clear inflation is approaching that target level:

“With lower energy prices and the stronger dollar likely to keep inflation below target for some time, it was noted that the Committee might begin normalization at a time when core inflation was near current levels, although in that circumstance participants would want to be reasonably confident that inflation will move back toward 2 percent over time.”

After these minutes were released, the center of gravity on the rate-hike timeline quickly shifted away from January and March to April (the Fed does not meet in February). It was actually quite foolish to think the Fed would increase rates in January or March, considering that Janet Yellen herself said rate increases would not occur until approximately six months after the end of QE. That program ended in October, and six months later places us in April.

My theory is that the Fed will need to see several months of increasing inflation—-ideally due to an expanding economy—before it considers raising rates. The likelihood of this occurring in 2015 is still pretty high.

If it does happen this year, it will be later than sooner, and probably not until September’s meeting at the earliest. This is because in the short-term, rising inflation seems unlikely, particularly because the recent plunge in oil and the rising strength in the US dollar are both anti-inflationary. Furthermore, the latest jobs numbers released last Friday showed that despite more hiring the average hourly wage declined. This too is anti-inflationary, and it does not bode well for an economy that should be improving and gearing up to embrace rate-hikes.

One would think that in the face of all this noise about the Fed raising rates, some would begin to doubt the consensus. Perhaps not so surprisingly, that doubter is the “Bond King” Bill Gross himself. He was recently quoted saying he believed the Fed might not raise rates in 2015, citing oil, the US dollar, and weak global economies as reasons why.

By the way, all this talk and debate about Fed policy surrounding “rates” actually only refers to one specific interest rate: the federal funds rate, that is currently at 0.25%. This is the rate at which banks and similar institutions trade their balances held at the Federal Reserve on an overnight basis and without collateral. In other words, this is the shortest term rate, and it is the only interest rate the Federal Reserve has direct policy control over.

The reason why analysts outside the small circle of institutions that actually interact with the federal funds rate care about it is so deeply is because raising or lowering it usually has a ripple effect in the same direction on all other longer term rates, like the discount rate, U.S. bond yields, and mortgage rates. Equity and debt markets, both domestic and foreign, are all affected by the raising and lowering of the federal funds rate.

Essentially, the Fed’s decision to raise rates has a real impact on every single person in the country, from the “bond kings” down to the hourly wage earners. But don’t count on that rate hike coming any time soon.

Featured image here.

Follow Casey on Twitter @CaseyBreznick for more updates and discussion on economics, finance, and business topics.

Donations tax deductible

to the full extent allowed by law.

Comments

They can’t allow interest rates to go up much. With the national debt at over $18 Trillion, any increase will have a serious impact on the cost to service the debt.

The Fed policy will continue to benefit those in the equities and bond markets-those with money to invest-and hurts those, mostly the poor, the middle class and seniors who have money sitting in bank accounts earning almost nil interest on CDs. There is no incentive to save.

The Krugman’s want the middle class to consume and not save for the future or invest in the market so as to keep their phony-baloney Keynesian policy limping along. A fiscal policy, not unlike the Social Security scam, that is a Ponzi scheme of Madoff proportions, to be sure.

I see that hand: Will Obama Claus refund all of my community college costs that I paid for out of my own pocket? For the books I have bought and continue to buy with my own money and read to educate myself on every topic that interests me, including economics, physics, theistic evolution and genetics?

Recommended reading: George Gilder’s “Wealth and Poverty” and “Knowledge and Power: The Information Theory of Capitalism and How It Is Revolutionizing Our World” and “The Israel Test.” http://www.gilder.com/books/

Also, Peter Schiff’s “The Real Crash: America’s Coming Bankruptcy—How to Save Yourself and Your Country” purchase all these books through the LI Amazon link on this web page

http://www.amazon.com/The-Real-Crash-Americas-Bankruptcy-How/dp/1250004470

anyone who believes that inflation is *only* 1.2% hasn’t been grocery shopping in awhile…

prices are up and package sizes are down on most items. for example, just try and find a half gallon of ice cream, or a 5 pound bag of sugar at the store: they’re 1 1/2 quarts and 4#s these days, but the prices are higher as well, and don’t get me started on the price of meat.

we’re being lied to, cheated & swindled on a daily basis, and it’s only going to get worse. sooner or later, the whole rotten house of cards is going to implode and if our alleged ruling class isn’t starting to worry about riots in the streets and being hunted down by angry mobs, they’re even dumber than i think they are, and that’s damn dumb.

The CPI is not an all-encompassing way to measure inflation.

As you note, it does not include many foodstuffs and doesn’t factor energy. However, it is still the most-cited inflation measure.

We know that. The point is that if the data is bad, how can the analysis be any good?

Outside of rent/mortgage payments the two big items in most household budgets are food and energy costs. No one can avoid paying for these items. Yet our decision makers have decided that these items should not be in the most widely used measure of inflation.

This is deceitful. The guestion is who are they lying to? The voters? Of to themselves?

“[H]ow can the analysis be any good?”

The point is not whether CPI is a good or bad measure of inflation, because it is such a measure. We all seem to agree it’s not a very good one, but that doesn’t change the fact that it measures inflation.

The Fed uses CPI in its models and considerations, so that is why I use it, and why almost every financial analyst and economist uses it (at least in discussion about Fed policy). Thus, if you’re interested in analyzing and thinking about Fed policy you have to swallow your pride and use CPI numbers.

The same goes for the official unemployment rate, U3, which is most cited. It is seriously flawed, but you still have to acknowledge it and consider it when analyzing institutions that use it as their basis of unemployment analysis.

Congress should mandate that inflation will be measured solely on the price of tofu.

Sure, it’s a terrible metric but at least we’ll all be using the same broken yardstick.

LOL

Their CPI is certainly relevant to what dove Yellin will do, and knowing it is a poor estimate of real inflation is important to know what to do as an individual. We can add in “hedonic pricing” to the list of distortions that help the fed get lower inflation. Deflation would be good for savers, our spendthrift politicians can’t allow that.

Massive debt (maybe $100T counting unfunded liabilities?) means the only way out seems to be printing their way out, and a slow economy may help prices stay a little lower, preventing panic. The USD still looks like the strong man in the world, but all currencies seem to be inflating.

Some guys say to watch for when rates start to rise despite QE4 efforts to keep them low, which would indicate bond vigilantes, or whoever, are starting to sell, rather than just not buying. The federal reserve is holding maybe $4T in debt, but couldn’t stop a global sell off.

I don’t really have the scope to say anything for sure, but the debt bomb seems like the real WMD, as I think even one military guy stated not long ago. Supposedly there is not so much leverage in the “game” now, but then I hear other views on that as well, that there are new ways the players are leveraging.

The price of hamburger is at record levels. The cheapest cuts of beef are now beyond the reach of many.

Ham is always a big sales item at New Years. Last year the cheapest brand on ham in my Supermarket- the plain rind on, bone in minimally processed cut where the trimmings and bone ends up on the stock pot as the base for soup, was on sale for $.99/lb. That had been the sales price for several years running. This year the very same ham was on sale for New Year’s at %1.89/lb- close to double.

The Fed will never raise rates voluntarily because doing so would destroy the US budget. With an $18 trillion dollar debt, every percentage point increase translates into $180 billion increase to service the debt. We do not have that money so the rate will remain near zero.

>

But as the rate is forced to remain near zero, inflation will increase. It already has and sites such as shadowstats.com and zerohedge.com place true inflation much higher than the official rate. Once again, the government has a vested interest in keeping the official inflation rate near 1% because every percent increase means much higher payouts for welfare which cannot be afforded.

>

Eventually inflation will become so apparent that the government must acknowledge it which means that interest rates must be raised as well. When this occurs, expect the wheels to come off the bus and the economy tanks.

Yep!

Raising rates only affects future debts, not past debts.

The fed has continually rolled the new debt into short term debt, not long term debt. These short-term debts are at lower rates than long-term debt, but are not paid off and instead are rolled again into short term debt. Thus we have a mountain of debt that will be affected by a change in the interest rates. Just another gift from the tax-cheat Geithner that will keep on giving.

I’m not entirely sure what you mean. You might be factually correct (I honestly don’t know), but your writing doesn’t make any sense.

Also, the Fed doesn’t pay the government’s debts, the U.S. Treasury does.

And just to nip this in the bud: While the Fed sets the interbank lending rate, and not explicitly the yield of T-bills, T-bills are in competition for investor dollars so they must eventually approach the same rate.

This is why the 10 year bill hit 15% in 1981/82: it was in competition with the Fed funds rate of 15%.

They’ll have to raise rates eventually, but they’re trying to stall until a Republican is president, so they can blame what follows on him or her.

Yellen has shown her partisan bias and will never raise rates so long as there’s a chance of it making Obama’s economy look bad.

Interest rates should be a market based determination of the time value of money. The Feds insistence that it is allowed to arbitrarily set rates is one of the prime causes of the boom and bust cycle. Setting the rates low, especially with the deduction for loses, leads to bad investment decisions that further exacerbates these cycles.