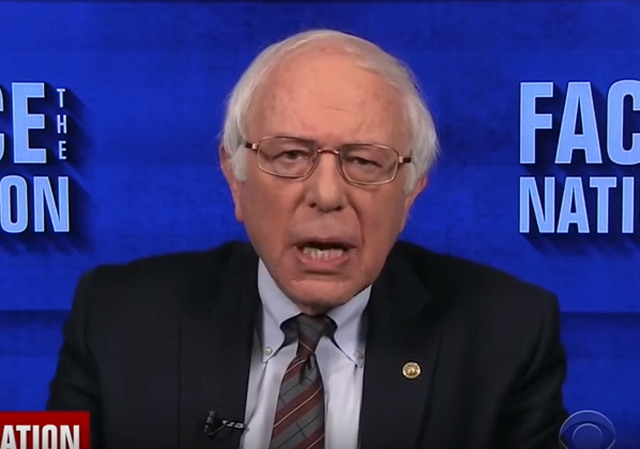

Bernie Sanders: Corporate Taxes Will ‘Absolutely’ go up if Dems Take Over

on December 18, 2017

17 Comments

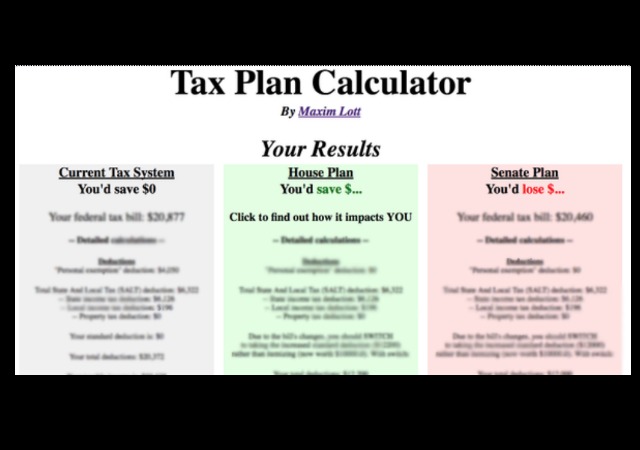

Bernie has been helping Democrats advance the narrative that the GOP tax reform bill is a big break for the wealthy and no good for the middle class. Yet Sunday on Face the Nation, Sanders admitted an inconvenient truth.