Stop the presses: the percentage of people without health insurance

has dropped in the first quarter of 2014.

But if a decline in the uninsured rate hadn't occurred when Obamacare began, now

that would have been a shock. After all, if you give Medicaid to a whole new group of people, offer subsidies to a huge number of other lower-income people, and stick everyone else with penalties for not getting insurance, it could be expected that the rate of those without health insurance would go down.

And I don't recall (although I could be missing something) that anyone on the right was suggesting that the total rate of the medically uninsured would fail to go down as a result of Obamacare.

The real questions were and are (a) how

much of a dent it would actually make in the uninsured (a figure that was probably somewhat elusive to begin with); (b) at what cost, both in money and disruption; (c) what quality of insurance would be the result; (d) what the effect on our health care system would be over time; and (e) the effect on our liberty.

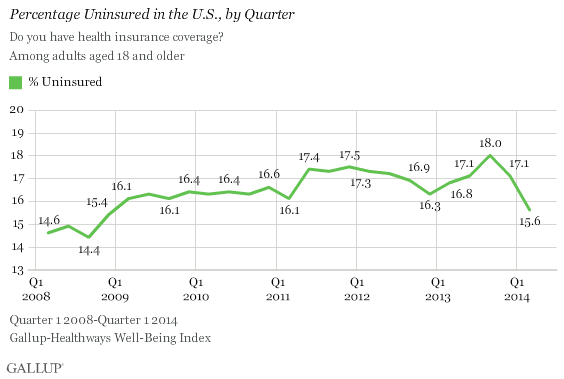

But anyway,

here are the stats are from Gallup. Unfortunately, I can't find a link to the actual study, and I always prefer to look at the more complete picture, but let's look at the chart from the summary version: