Unemployment Claims Hit 6.6 Million Last Week Due to Wuhan Coronavirus Pandemic

on April 09, 2020

11 Comments

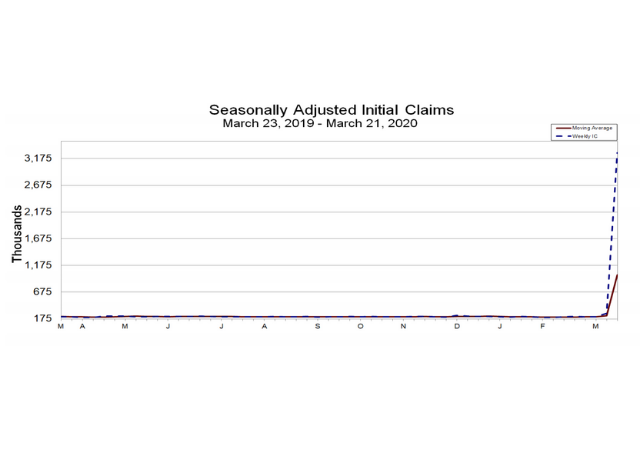

The Labor Department reported that 6.6 million Americans filed for unemployment between March 28 and April 4.