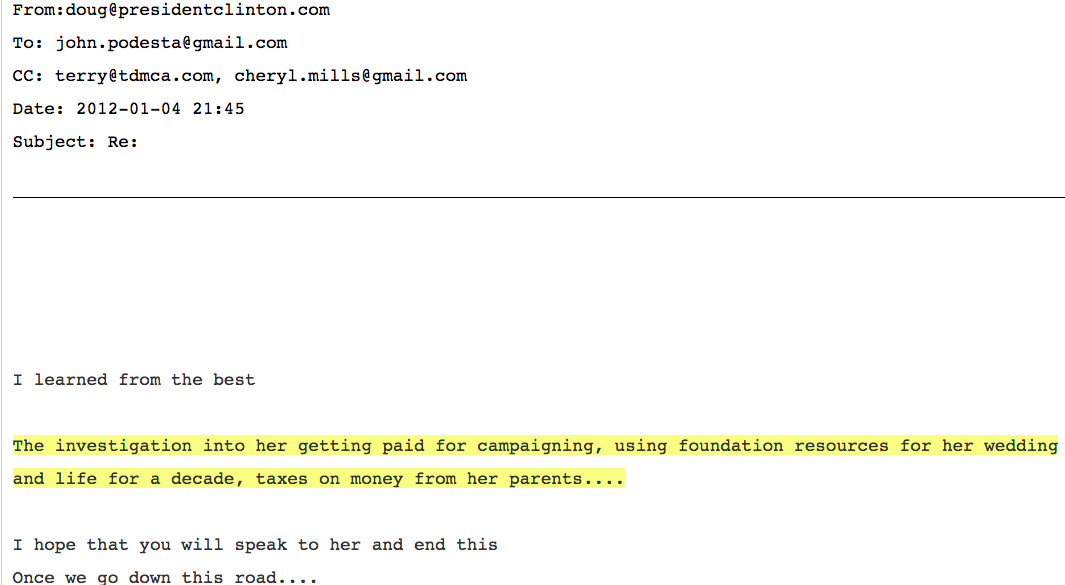

Oh boy. PAGING THE IRS! The list of wrongdoings with the Clinton Foundation continues to grow. Another Wikileaks dump shows one Clinton aide accusing Chelsea Clinton of using Clinton Foundation funds to pay for wedding among other things:

This is just the latest piece of the drama between Doug Band, President Clinton’s personal assistant in the 1990s and founder of Teneo, and Chelsea Clinton, which could only fuel problems with the foundation.

Band was not too pleased that Chelsea told one of President George W. Bush’s daughters about her intentions because the daughter then leaked the story to a Republican operative.

Band was willing to do all that was necessary to protect himself from Chelsea’s accusations. He even offered an 11-page memo that spilled the ways President Clinton used the foundation for personal profit and how his company Teneo encouraged its clients to donate to the foundation.

About a month after Band sent out the memo, Simpson, Thatcher & Bartlett LLP contacted Podesta its draft of an audit of the Foundation. It found:

The audit draft noted substantial issues, including a Conflict-of-Interest Policy that had not been implemented, conflicts that were not disclosed in a timely fashion and board members not following the policy when they became aware of conflicts.“In addition, some interviewees reported conflicts of those raising funds or donors, some of whom may have an expectation of quid pro quo benefits in return for gifts,” according to the Dec. 5, 2011, draft. Another section of the document noted that “interviewees also mentioned instances in which gifts and payments received by staff had not been properly disclosed.”There were other problems, including 1,298 “complimentary” $20,000 memberships for the Clinton Global Initiative as opposed to just 500 paid memberships. Of the “complimentary” group, “276 were coded ‘discretionary,’” the audit noted.“Interviewees informed us that there is no transparency into how the comp list is developed,” the document stated.The lawyers conducting the audit also noticed problems in the Foundation’s IRS Form 990, the tax return document of an organization that is exempt from income tax. While charitable groups are allowed to pay board members and staff a reasonable salary, none of the reasonable compensation calculations identified by the lawyers were ever done, the 990 form showed. The lawyers also wrote the 990 indicated the Foundation had a written conflict-of-interest policy that was enforced.“However, we did not find evidence of that enforcement,” the memo stated.

It turns out the IRS has sniffed around the foundation. As Kemberlee noted on Friday, an IRS office in Dallas has decided to look into the Clinton Foundation and why it still holds a tax exempt status. If what Band says is true, then yes there is a case against the Clinton Foundation:

Using a nonprofit group for personal enrichment — called inurement — is one sure-fire way to gain IRS scrutiny.In the case of the Clinton Foundation, it’s not exactly a matter of stealing from the cookie jar. The bookkeeping — with documents available for public as well as IRS scrutiny — appears sound since the IRS has not raised any red flags. The foundation spends a solid 88 percent of its money on actual programs, according to the group Charity Tracker. That’s pretty good ratio of overhead to actual charity work.But the Clinton Foundation problem is more nebulous. The central question is not exactly one the IRS can easily track: Did the founding members trade influence for donations, especially while Hillary Clinton was secretary of State?Clinton and her staff have consistently denied any conflicts of interest or improper enrichment and cite reporting holes in the media stories and books claiming pay-to-play relationships. But since July, more information has been revealed, via hacked email correspondences of Clinton adviser John Podesta released by Wikileaks.The emails reveal that Chelsea Clinton ordered an audit of the foundation and “some interviewees reported conflicts of those raising funds or donors, some of whom may have an expectation of quid pro quo benefits in return for gifts.”Given this language, citing “gifts” and “quid pro quo benefits” in emails is a pretty bad move for anyone involved in a nonprofit group. Another bad move: When senior Clinton advisers like Doug Bland call the intersection of the foundation fundraising and the former president’s personal activities “Bill Clinton Inc.”

No word yet if Band’s email will have an impact on the IRS investigation.

CLICK HERE FOR FULL VERSION OF THIS STORY

{kind=link}