Entering 2015, most economists expected that the Federal Reserve would finally begin raising short-term interest rates. Fewer than two weeks in to the year and that thesis is already beginning to crumble.

For seven years, the Fed kept interest rates at rock-bottom levels and employed a massive money-printing program called Quantitative Easing in the hopes of boosting the money supply, expanding credit, and causing inflation to jump-start the economy (so the theory goes). Many experts have long waited for the Fed to “normalize” policy and raise rates, for reasons that include a desire to stop expanding the money supply, and wanting the Fed to have a cushion to lower them once again when another crisis occurs.

While credit finally appears to be coming more available, neither the mild-mannered inflation the Fed wanted nor the rampant hyperinflation Fed detractors prophesied has materialized.

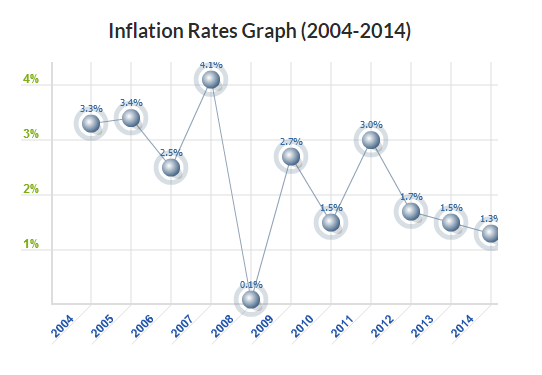

In 2014 the CPI inflation rate was 1.3%, the lowest since 2008. However, most economists, including those at the Fed, like to see 2% inflation.

Inflation has decreased every year since 2011, when it registered at 3%, and hasn’t been at or above the 2% target since then. This trend does not inspire confidence in Fed policy makers to increase rates right now.

Still, the minutes released by the Fed on Jan. 7 indicate the Fed does not need to see 2% inflation to begin raising rates. What they do indicate is that the Fed will not raise rates until it becomes clear inflation is approaching that target level:

“With lower energy prices and the stronger dollar likely to keep inflation below target for some time, it was noted that the Committee might begin normalization at a time when core inflation was near current levels, although in that circumstance participants would want to be reasonably confident that inflation will move back toward 2 percent over time.”

After these minutes were released, the center of gravity on the rate-hike timeline quickly shifted away from January and March to April (the Fed does not meet in February). It was actually quite foolish to think the Fed would increase rates in January or March, considering that Janet Yellen herself said rate increases would not occur until approximately six months after the end of QE. That program ended in October, and six months later places us in April.

My theory is that the Fed will need to see several months of increasing inflation—-ideally due to an expanding economy—before it considers raising rates. The likelihood of this occurring in 2015 is still pretty high.

If it does happen this year, it will be later than sooner, and probably not until September’s meeting at the earliest. This is because in the short-term, rising inflation seems unlikely, particularly because the recent plunge in oil and the rising strength in the US dollar are both anti-inflationary. Furthermore, the latest jobs numbers released last Friday showed that despite more hiring the average hourly wage declined. This too is anti-inflationary, and it does not bode well for an economy that should be improving and gearing up to embrace rate-hikes.

One would think that in the face of all this noise about the Fed raising rates, some would begin to doubt the consensus. Perhaps not so surprisingly, that doubter is the “Bond King” Bill Gross himself. He was recently quoted saying he believed the Fed might not raise rates in 2015, citing oil, the US dollar, and weak global economies as reasons why.

By the way, all this talk and debate about Fed policy surrounding “rates” actually only refers to one specific interest rate: the federal funds rate, that is currently at 0.25%. This is the rate at which banks and similar institutions trade their balances held at the Federal Reserve on an overnight basis and without collateral. In other words, this is the shortest term rate, and it is the only interest rate the Federal Reserve has direct policy control over.

The reason why analysts outside the small circle of institutions that actually interact with the federal funds rate care about it is so deeply is because raising or lowering it usually has a ripple effect in the same direction on all other longer term rates, like the discount rate, U.S. bond yields, and mortgage rates. Equity and debt markets, both domestic and foreign, are all affected by the raising and lowering of the federal funds rate.

Essentially, the Fed’s decision to raise rates has a real impact on every single person in the country, from the “bond kings” down to the hourly wage earners. But don’t count on that rate hike coming any time soon.

Featured image here.

Follow Casey on Twitter @CaseyBreznick for more updates and discussion on economics, finance, and business topics.

CLICK HERE FOR FULL VERSION OF THIS STORY

{kind=link}