Did Chelsea Use Clinton Foundation Funds to Pay For Her Wedding?

The case against the Clinton Foundation misusing funds grows.

Oh boy. PAGING THE IRS! The list of wrongdoings with the Clinton Foundation continues to grow. Another Wikileaks dump shows one Clinton aide accusing Chelsea Clinton of using Clinton Foundation funds to pay for wedding among other things:

This is just the latest piece of the drama between Doug Band, President Clinton’s personal assistant in the 1990s and founder of Teneo, and Chelsea Clinton, which could only fuel problems with the foundation.

Band was not too pleased that Chelsea told one of President George W. Bush’s daughters about her intentions because the daughter then leaked the story to a Republican operative.

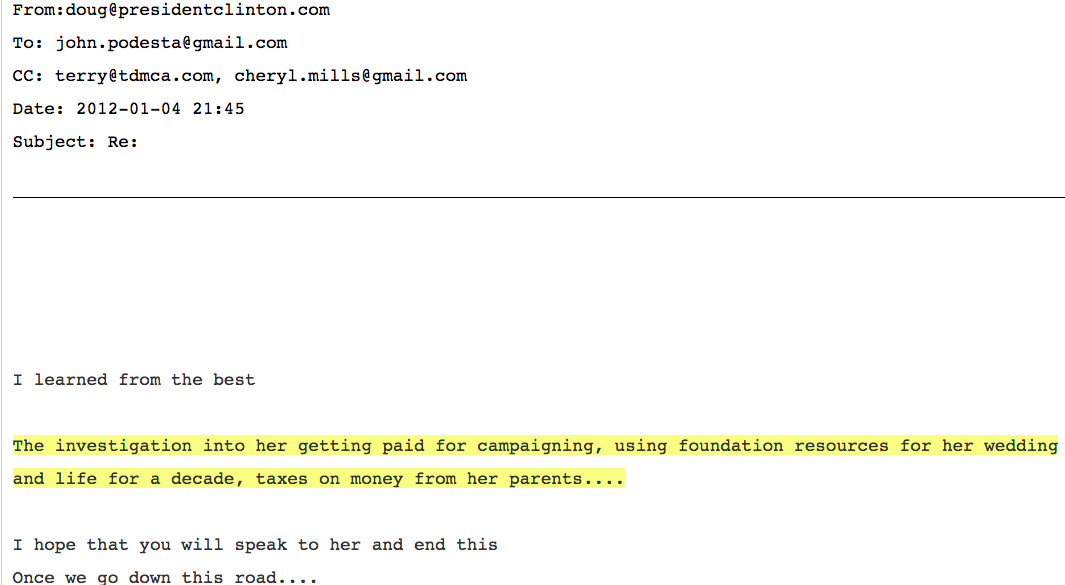

Band was willing to do all that was necessary to protect himself from Chelsea’s accusations. He even offered an 11-page memo that spilled the ways President Clinton used the foundation for personal profit and how his company Teneo encouraged its clients to donate to the foundation.

About a month after Band sent out the memo, Simpson, Thatcher & Bartlett LLP contacted Podesta its draft of an audit of the Foundation. It found:

The audit draft noted substantial issues, including a Conflict-of-Interest Policy that had not been implemented, conflicts that were not disclosed in a timely fashion and board members not following the policy when they became aware of conflicts.

“In addition, some interviewees reported conflicts of those raising funds or donors, some of whom may have an expectation of quid pro quo benefits in return for gifts,” according to the Dec. 5, 2011, draft. Another section of the document noted that “interviewees also mentioned instances in which gifts and payments received by staff had not been properly disclosed.”

There were other problems, including 1,298 “complimentary” $20,000 memberships for the Clinton Global Initiative as opposed to just 500 paid memberships. Of the “complimentary” group, “276 were coded ‘discretionary,’” the audit noted.

“Interviewees informed us that there is no transparency into how the comp list is developed,” the document stated.

The lawyers conducting the audit also noticed problems in the Foundation’s IRS Form 990, the tax return document of an organization that is exempt from income tax. While charitable groups are allowed to pay board members and staff a reasonable salary, none of the reasonable compensation calculations identified by the lawyers were ever done, the 990 form showed. The lawyers also wrote the 990 indicated the Foundation had a written conflict-of-interest policy that was enforced.

“However, we did not find evidence of that enforcement,” the memo stated.

It turns out the IRS has sniffed around the foundation. As Kemberlee noted on Friday, an IRS office in Dallas has decided to look into the Clinton Foundation and why it still holds a tax exempt status. If what Band says is true, then yes there is a case against the Clinton Foundation:

Using a nonprofit group for personal enrichment — called inurement — is one sure-fire way to gain IRS scrutiny.

In the case of the Clinton Foundation, it’s not exactly a matter of stealing from the cookie jar. The bookkeeping — with documents available for public as well as IRS scrutiny — appears sound since the IRS has not raised any red flags. The foundation spends a solid 88 percent of its money on actual programs, according to the group Charity Tracker. That’s pretty good ratio of overhead to actual charity work.

But the Clinton Foundation problem is more nebulous. The central question is not exactly one the IRS can easily track: Did the founding members trade influence for donations, especially while Hillary Clinton was secretary of State?

Clinton and her staff have consistently denied any conflicts of interest or improper enrichment and cite reporting holes in the media stories and books claiming pay-to-play relationships. But since July, more information has been revealed, via hacked email correspondences of Clinton adviser John Podesta released by Wikileaks.

The emails reveal that Chelsea Clinton ordered an audit of the foundation and “some interviewees reported conflicts of those raising funds or donors, some of whom may have an expectation of quid pro quo benefits in return for gifts.”

Given this language, citing “gifts” and “quid pro quo benefits” in emails is a pretty bad move for anyone involved in a nonprofit group. Another bad move: When senior Clinton advisers like Doug Bland call the intersection of the foundation fundraising and the former president’s personal activities “Bill Clinton Inc.”

No word yet if Band’s email will have an impact on the IRS investigation.

DONATE

DONATE

Donations tax deductible

to the full extent allowed by law.

Comments

How much did she have to pay the guy?

A Saudi Arabian dowry

Three camels and a goat. At first the groom was elated. He thought he had received an extra goat, praise allah. But upon closer examination he found the bride was standing next to the goat…hence the need for a burka (to tell one from the other during daylight hours). Thankfully, they’re easy to find in Manhattan.

Burka’s or goats? Both.

Grifters gonna grift.

“Yeah, you may say you want to audit the company, but maybe you ain’t thought things through, little lady. Sure, there’s some under the table dealing and skimming going on, but your pretty little hands are just as dirty as any of ours, and if we have to go down because of this, you’re going down right beside us.”

–The Godmother, Part II

Staring Hillary, and opening in 2017.

“No word yet if Band’s email will have an impact on the IRS investigation.”

There could be more than that. We’re lucky Comey is so inept he didn’t even know how to run a fake investigation. He and Lych were so boresighted on preventing the field agents from having the tools they would normally have in a real investigation Comey left a lot of stones unturned. In other words, while he was making sure the investigation was going to be a pure whitewash of Clinton, he left a lot of evidence lying around for others to find. And the NYPD, which was actually conducting a real investigation, found it and now it’s outside the feds’ control.

Had Comey at least allowed his agents to get search warrants, search the subjects’/material witnesses’/whatev’s homes he would have had that laptop before anyone else could get to it. And right now it would be locked up in the same government warehouse where the Ark of the Covenant has been stored, never to see the light of day again, since Indiana Jones stole it back from the Nazis.

Comey may be a good lawyer, but he sure didn’t impress me as such during his various testimonies before Congress when he was acting as Hillary Clinton’s defense attorney. He wrote in an impossibly high intent standard and then argued he couldn’t recommend prosecution unless that standard was met. He’s not the first idiot to think of that. Others who have been prosecuted and convicted of violating 18 U.S.C. 793(f), which requires the prosecution to prove just gross negligence, have tried the same thing. And as I said that argument was laughed out of court. The federal appeals courts have ruled that they were convicted under the exact section of the statute that covered their criminal misconduct, that those sections exist for a reason, and that Congress’ intent was clear when they wrote them. They exist to provided a hierarchy of punishments depending on one’s degree of culpability. The prosecution does not have to prove a higher degree of culpability as long as they correctly charged the defendant in the first place.

I digress but only slightly. Comey hasn’t impressed me as a lawyer, but he’s a complete clown as an investigator.

So now the NYPD has turned over at least one stone Comey wouldn’t let his agents turn over. Now they have everything. There is likely to be a lot of information about the Clinton foundation and its misuse of funds in that cache of 650k emails. In fact it’s highly likely. If so, there would be evidence of crimes committed under state law not just federal.

So now that James Comey and Loretta Lynch have lost control of the evidence they’ve also lost control over any prosecutions that may result. If there’s evidence that Chelsea Clinton as well as other Clintons were using foundation money as the family slush fund we all know it is (I believe the last tax filing on record shows that only 5.76% of the expenses for the year went to bonafide charitable activities) there be several felony level violations of state law such as fraud.

That, by the way, is another mark of a professional investigation vs. farcical, Potemkin pretense of an investigation Comey was putting on. Investigations always expand. They were at first only investigating Weiner over his underage sexting. But now the NYPD (and the feds; the FBI and US District Attorney for the Southern District of NY are involved too, and it appears these FBI agents are among those royally P.O.d at Comey) has developed leads to other crimes. That always happens in a genuine investigation. It happen in Comey’s fake one. They couldn’t even make the slam dunk case that Clinton violated the Federal Records Act because of Comey. Remember how he bragged about his personal involvement in the investigation? He was personally involved to make sure that agents didn’t follow leads. He was riding herd on those agents to make sure the investigation remained as narrowly focused as possible; i.e. only the question of mishandling classified material. This does not happen in real life. This only happens in “investigation theater.”

So, tonight hoist one and toast the fact that James Comey is a rank amateur who didn’t know how far out of his depth he was. I wonder what might be on other computers the NYPD might be able to seize because Comey’s sloppy, inept fakery didn’t bring them under federal control.

New York Magazine has a different take. Maybe you are right – just saying there are other points of view. http://nymag.com/daily/intelligencer/2016/10/by-the-way-the-fbi-was-investigating-the-clinton-foundation.html

That’s not really a very different perspective. I said:

“[I]t appears these FBI agents are among those royally P.O.d at Comey.”

They said (amongst other things):

“FBI agents continued probing the foundation using methods that did not require Justice Department approval.”

Basically we’re saying the same thing; we’re talking about FBI agents bound and determined to go where the evidence leads even if their bosses don’t like it. We just mentioned different bosses.

Where we differ is why they’re doing it. In classic liberal projection, since all things are political in their world, the writers at the NY Mag think these FBI agents must be doing it for political reasons. They must be part of the VRWC out to get poor innocent Hillary.

We’re talking about people who know their newspapers’ motto like “All The News That’s Fit to Print” or “To Give The News Impartially, Without Fear or Favor” is a joke. Nothing to be taken seriously; they’re unrepentant political hacks. They can’t conceive of the idea that there really are FBI agents who regardless of how they vote actually do take the FBI’s motto “Bravery, Fidelity, Integrity” seriously. Who value their reputations more than they value any short term partisan advantage.

Their reputations, the FBI’s reputation, wasn’t Comey’s to give away. He’s not a career agent; he’s a political appointee. Yet he did. Hence the growing mutiny. And as I said the people at NY Mag, and in most of the media, the idea of people valuing their integrity over political affiliation is simply inconceivable.

BTW, we’re talking about two different investigations. The investigation into Weiner’s sexting and the Clinton foundation are two different investigations. My point about professional investigations is this. You just never know what you might uncover, if you’re given the tools and are allowed to follow the leads. One investigation can uncover leads that aid a different, separate investigation.

1st, cut the BS about “classic liberal projection”. Projection know no partisanship. I see plenty of projection right here on this site. It is insulting. People are projecting about fraud because Trump is going to lose. They are projecting that the media is biased because the coverage isn’t the way they would like. This site does more projecting than the NYTimes.

The FBI motto means nothing. Hoover came up with it and he showed little bravery, fidelity or integrity. He was a bully and a blackmailer. In particular, he was rather selective in whom he pursued. He denied the mafia existed and tried to destroy the civil rights movement. Whether he was a homosexual remains open to speculation.

2nd, that is not how I read the NY article. I read it as superiors saying the case was thin and the prosecutors saying they didn’t see enough to prosecute. The agents were told to move on to something more promising. Big difference. Perhaps you and the agents are doing the projecting and the superiors were doing their job. As this article quotes, the Clinton Foundation gets a top rating from the charity watchdogs. You can read the rest for yourself.

In Hollywood movies, the dogged investigator always has to fight the bad guys and his superiors. In real life it doesn’t always play out that way. Sometimes the superior, is, well, superior. As for Comey, he is their boss. That is how it works. The elected or appointed have been chosen or picked indirectly by the electorate. That is done specifically so that the permanent staff do not become a law onto themselves. When Douglas MacArthur tried to defy Truman, he was fired. Then he tried to run for office and got nowhere.

These agents were bound and determined, but whether they are following the evidence has yet to be determined. Maybe they are out to get Hillary. The Clintons have been under near constant investigation for 25 years and all of those investigations led to a stain on a blue dress. Do you think you could stand up to that kind of investigation?

‘Their reputations wasn’t Comey’s to give away”? What about the chain of command? Where is the Inspector General or whoMever is ombudsman in the FBI? That is where you go when you have a disagreement with your boss. You don’t leak to Giuliani – who is absolutely a partisan. Giuliani couldn’t help from opening his big mouth and giving the game away. He tried to take it back, but he couldn’t.

Again with the insults about liberals being unable to value integrity. I seem to remember Reagan trading arms for hostages. I could come up with 25 more examples, if I wished. But you would deny each and every one of them was a ‘true’ conservative. That is why I chose Reagan.

“if you’re given the tools and are allowed to follow the leads” or going on a fishing expedition. Ken Starr started out looking at Whitewater. Since he only had 1 guy to investigate, he didn’t stop when he came up cold. 3 years later he came to Paula Jones. There is reason to believe there was no there there with Paula Jones, either. Her husband, to whom she was not married at the time she met Clinton, was jealous. A bunch of right-wing haters including Ann Coulter fed the flames. The rest is bad history.

As I already pointed out, Obama and Cuomo should pardon the Clintons to avoid 4-8 years of old squabbling. You could start some fresh persecutions. At least both sides would start out even. The bookies and the polls say Clinton will be President.

We can’t afford to continue this. She is not taking anyone’s guns away – Obama didn’t even try. But abortion will remain legal. You can’t stop either one. There is an ulcer medication that women in Mexico take. It is 80% effective in the 1st trimester. There is always the coat hanger or women throwing themselves down stairs. Sound enchanting. Besides NY and CA have laws that go into effect the minute Roe v. Wade is overturned. Rich women will get them. They will fly to NY. Poor woman won’t. Then the poor woman’s child will get a shitty education and might grow up to use a gun.

Impressive. All I an do is paraphrase the Bard.

“It is a word salad

Spewed by an idiot, full of sound and fury,

Signifying nothing”

@Arminius Please address at least this one point. If the agents were just doing their job, why did they break the law and spill to Giuliani? If you can’t answer that, then your ‘paraphase’ is just deflection.

I doubt the bard would appreciate you paraphrasing him. But as we used to say in Brooklyn, you got nothin’ and your calling me an idiot emphatically says you got nothin’.

I was impressive and as we would repeat in Brooklyn, you still got nothin’.

I addressed everyone one of your points and apparently, you got nothin’.

So I guess you are going to shut up on this topic since you got nothin’.

They didn’t “spill” and go to Giuliani. Giuliani tried to be careful and distinguish between retired and current agents. He said repeatedly he would not talk to currently serving agents as he didn’t want to put them in a compromising position. One slip of the tongue and you want a federal investigation. But the reams of evidence against the Clintons? All fine with you.

You are despicable. You have no principles. I said months ago that these FBI agents who wanted to maintain their integrity after Comey betrayed it would have to be very careful. Because partisan shitheels like you would be out for blood for because your sacred cows would have been gored. They wouldn’t be able to go to the IG because neither the IG nor a Republican Congress can protect whistle blowers from people such as you, when you’re in power.

They clearly couldn’t go to CNN or the NYT or the WaPo. Sure, when the Pres has an R after his name, the the only important thing is what the patriotic whistle blower has to say. But when the Pres has a D after his name the only important thing is, how can we expose this traitor. And now you sharks and sea snakes want to know why thy didn’t come to the likes of you?

If Hillary wins, this is all irrelevant. Nobody would dare touch her or her family.

If Trump wins, the investigation of the Clintons will be one of the highlights of the century.

IIRC, a presidential pardon only extends to criminal punishment. Civil liabilities – as in the fraudulent tax benefits garnered by a fraudulent “Foundation” are not subject to pardon.

Do bears poop in the woods???

Have the Clinton(s) ever…

1. Paid for anything with their own money?

2. Told the truth?

3. Accomplished anything beneficial for the taxpayer/voter?

IOW, their value to humankind is ZERO!

The whole family is scum.

tRumps siblings are fine people.

Careful Rags, you’re going to out your sockpuppet if both of you happen to use the same grade-school nicknames to demean Trump.

Kinda like when someone routinely uses the term “collectivist” to complain OnlyRightDissentAllowed. Gosh golly what a coincidence that would be.

You actually get to vote? I wish we had a rationality test. Rags doesn’t even like me. The few times I tried to find common ground, he rejected me. I just liked the tRump construction and I adopted it. Isn’t the point of commenting to spread your ideas?

But I can call you a Trumputian. That is my own construct. I wonder if you can guess where it comes from. Rags is welcome to adopt it. I have a feeling you will still be one long after tRump has retreated into his Tower. He may have to change his name back to Drumpf.

Fen, two things…

You’re intentionally conflating me with another poster. That’s one of your little crap-weasel lies. Nobody here posts under more than one moniker.

ORDA doesn’t even post in a style remotely like mine. Any half-bright monkey can measure the length of my average post and his, and know they are NOT by the same person.

I don’t have the kind of time it would take to write what he does on a thread, being that I actually do practice law as a solo practitioner.

You lying little sack of filth.

Actually they are. No one’s been able to cite a single instance of bad behavior by any of the trump children.

I was referring to DJT’s siblings. But I will accept that. Unfortunately, Donald J. Trump is deplorable and he is the one running.

Get back to me when the Trump Foundation gets a report from Charity Tracker that he spends anywhere near 88 percent of its money on actual programs. Get back to me when he does 5% of the good that the Clinton Foundation does. Get back to me when the IRS actually takes an action.

Get back to me when tRump releases his tax returns – audited or not. They can’t all be under audit. The IRS can only go back 3 years unless there is an allegation of fraud. Where is his 2012 return?

How do you know the whole thing isn’t forged? That is the Russians M.O. They start with legitimate traffic and then they send in the forgeries.

So who’s the next suspect, the Jews? Christians? The NRA?

What a blatant leftist troll.

How do you know that some of the WikiLeaks documents aren’t forged – regardless of where they came from? How do you know?

Not only that , but Hillary stole the silver from the reception / High Plains Grifter

So what didn’t we know about the use of the Clinton Crime Family Charity & Massage Parlor before this Chelsea wedding dress story. I am sure that many other things were purchased from the fund distributions to its fund administrator.

In fairness, however, we are not giving equal time to the Trump Foundation which has been used to bribe politicians ($100,000 to the Clinton Foundation for unspecified benefits and Florida’s AG Pam Bondi’s campaign fund during the time her office was considering legal action against Trump University); $100,000 to settle a lawsuit with Palm Beach involving Mar-a-Lago and the purchase a Donald Trump portrait for $20,000.